Secure payment gateway guide for UK ecommerce

TL;DR:

- A secure payment gateway encrypts and transmits payment data, ensuring compliance with PCI DSS and SCA standards. Proper integration involves thorough checkout audits, strict script control, and secure webhook handling to prevent breaches and scope creep. Prioritizing these security measures protects transactions, maintains compliance, and minimizes revenue loss.

A secure payment gateway is a technology solution that encrypts and transmits payment data between your customer, your store, and the acquiring bank, protecting sensitive card details while meeting industry compliance standards. For UK and EU businesses in 2026, the stakes are higher than ever. PCI DSS 4.x, Strong Customer Authentication under PSD2, and EMV 3D Secure 2 have collectively raised the bar for what “secure” actually means in practice. This secure payment gateway guide cuts through the noise and gives you a clear, practical path from checkout architecture review to live, compliant payment processing.

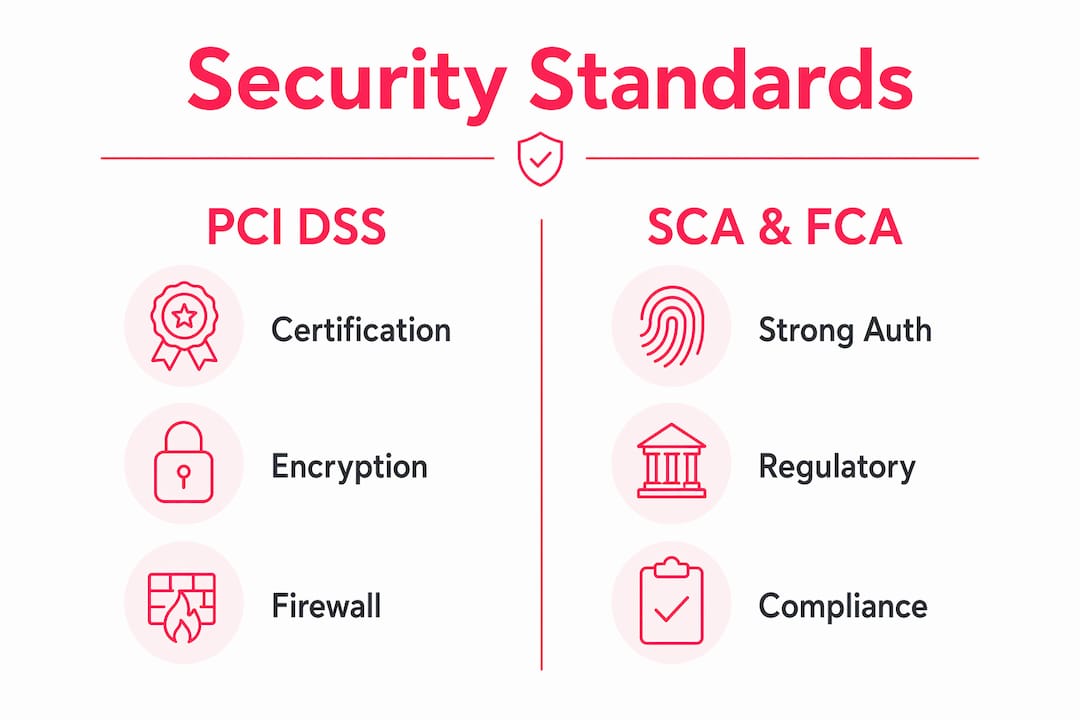

What are the essential security standards for payment gateways?

PCI DSS (Payment Card Industry Data Security Standard) is the non-negotiable baseline for any business processing card payments online. The version that matters in 2026 is PCI DSS 4.0.1, and it introduces meaningful changes to how merchants handle payment pages, not just cardholder data storage.

The most consequential shift for eCommerce merchants is around SAQ (Self-Assessment Questionnaire) eligibility. Merchants using fully hosted or redirected checkout pages may qualify for SAQ A, which is the lightest compliance tier. That sounds like good news, and it is, but there is a catch. Under PCI DSS 4.x Requirements 6.4.3 and 11.6.1, even SAQ A merchants must implement script inventories and tamper detection on their payment pages. Magecart-style attacks inject malicious JavaScript into checkout pages to skim card data before it ever reaches the gateway. Script control is your defence against that.

Here is what PCI DSS compliance requires you to address:

- Script inventory and authorisation: Every script running on your payment page must be documented and explicitly authorised.

- Tamper detection: Mechanisms must alert you if scripts are modified or new ones are injected without authorisation.

- TLS encryption: All payment data in transit must use TLS 1.2 or higher. TLS 1.0 and 1.1 are not acceptable.

- MFA for the CDE: Multi-factor authentication applies to all access into the cardholder data environment, including local and console access, not just remote logins.

Beyond PCI DSS, UK and EU merchants must comply with Strong Customer Authentication (SCA) under PSD2 and the UK FCA’s equivalent regulations. SCA requires two independent authentication factors, drawn from something the customer knows, something they have, or something they are. The primary technical mechanism for delivering SCA on remote card payments is EMV 3D Secure 2 (3DS2). Exemptions exist for low-risk transactions, but your gateway and integration must handle these correctly or you will see unnecessary friction and declined payments.

How to choose the best payment gateway for secure transactions

Choosing between payment gateways is not just a commercial decision. It is a security and compliance decision that shapes your PCI DSS scope for years.

The single most important variable is how the payment form is delivered. A hosted payment page, where the customer is redirected to a gateway-owned URL (as with PayPal’s standard checkout), keeps your servers entirely out of scope for card data. An embedded iframe solution, used by Stripe and Adyen, keeps the user on your site while the card fields are served from the gateway’s domain. Both can qualify for SAQ A, but only if your own scripts do not interact with the payment fields. Merchant-owned scripts influencing checkout can push you from SAQ A into SAQ A-EP, which carries significantly more controls and audit requirements. That is a material difference in compliance overhead.

When comparing gateways, evaluate them against these criteria:

| Criterion | What to look for |

|---|---|

| PCI DSS certification | Confirm the gateway holds a current PCI DSS Level 1 Service Provider certificate |

| 3DS2 support | Native EMV 3DS2 with soft decline handling and exemption management |

| Fraud detection | Built-in machine learning fraud scoring (Stripe Radar, Adyen RevenueProtect) |

| Webhook security | HMAC signature verification on all event notifications |

| TLS and encryption | TLS 1.2+ enforced, with tokenisation for stored payment methods |

Stripe and Adyen are the two gateways we see most frequently on well-architected UK eCommerce builds. Stripe’s developer experience is strong, its documentation for 3DS2 is thorough, and Stripe Radar provides solid baseline fraud detection. Adyen suits higher-volume merchants and offers more granular control over authentication flows and exemption logic. Both hold PCI DSS Level 1 certification.

Pro Tip: Before signing any gateway contract, request the vendor’s current Attestation of Compliance (AoC) document. This is the formal proof of their PCI DSS Level 1 status. Any reputable gateway will provide it without hesitation.

For a broader look at how different payment gateway solutions compare for UK retail, the security features section is worth reviewing alongside your shortlist.

Step-by-step guide to integrating a secure payment gateway

Integration is where most security problems originate. A gateway with excellent security credentials can still be implemented insecurely. Follow these steps to get it right.

-

Audit your checkout architecture. Map every script, third-party tag, and iframe on your payment pages. Identify whether any merchant-controlled JavaScript touches or reads payment fields. This determines your PCI DSS SAQ classification before you write a single line of integration code.

-

Implement a Content Security Policy (CSP). A properly configured CSP header restricts which scripts can execute on your payment pages. Combine this with Subresource Integrity (SRI) hashes for any third-party scripts you load. This is your primary technical control for Requirements 6.4.3 and 11.6.1.

-

Integrate 3DS2 authentication flows correctly. Your integration must handle three outcomes: frictionless authentication (the transaction passes without a challenge), challenge flow (the customer completes a step-up verification), and soft decline (the issuer requires SCA but your initial request did not include it). Soft declines and retries must be handled gracefully. A soft decline is not a failed payment. It is a signal to re-submit the transaction with a 3DS2 authentication request. Missing this step means lost revenue.

-

Secure your webhook handlers. Webhooks are how your gateway notifies your server of payment events. Webhook handlers must validate signatures using the raw request body bytes, before any JSON parsing or middleware transformation. This is a common mistake. If you parse the JSON first and then verify the signature, the signature check will fail in production. Deduplicate events by their unique event ID to prevent duplicate order fulfilment.

-

Enforce MFA on all administrative access. Every user account with access to your payment gateway dashboard, your eCommerce admin, and any system within your cardholder data environment must use multi-factor authentication.

-

Test end-to-end before go-live. Run through frictionless flows, challenge flows, and soft decline retries in your gateway’s test environment. Verify that webhook signatures validate correctly and that your idempotency logic prevents duplicate orders on retry.

| Integration step | Key security control | Common failure point |

|---|---|---|

| Checkout audit | SAQ classification | Undetected merchant scripts in payment fields |

| CSP implementation | Script tamper detection | Overly permissive CSP rules |

| 3DS2 integration | SCA compliance | Missing soft decline retry logic |

| Webhook security | Signature verification | JSON parsing before raw body verification |

| MFA enforcement | CDE access control | Limiting MFA to remote access only |

For a detailed walkthrough of secure payment integration steps specific to UK eCommerce builds, we have covered the technical specifics in depth.

Pro Tip: Use your gateway’s webhook testing tool to send simulated events to your local environment before deploying. Confirm that your raw body capture is working correctly by intentionally modifying the payload and checking that signature verification rejects it.

Common challenges when deploying secure payment gateways

Even well-planned implementations run into problems. Here are the issues we see most often, and how to resolve them.

Scope misclassification. This is the most expensive mistake. A merchant assumes SAQ A eligibility, submits their self-assessment, and later discovers that a single analytics tag or A/B testing script on the payment page has expanded PCI DSS scope to SAQ A-EP. The fix is a thorough pre-integration audit, not a post-launch scramble. Use browser developer tools to capture every network request and script execution on your checkout page.

Broken webhook signature verification. Using JSON middleware before verifying signatures breaks the trust chain because the provider’s signature covers the raw bytes, not the parsed object. The fix is straightforward: capture the raw request body as a byte stream before any middleware processes it, then verify the HMAC signature against those raw bytes.

3DS2 authentication failures. Missing challenge flows or incorrect exemption handling leads to declined transactions and frustrated customers. A secure 3DS implementation must handle soft declines, exemptions, and retries without losing the original order context. Build a state machine for your checkout flow that explicitly handles each 3DS2 outcome.

Treating webhook handlers as simple callbacks rather than replay-safe pipelines is a reliable way to end up with double-shipped orders and corrupted order states. Build idempotency in from day one.

Ongoing monitoring gaps. Compliance is not a one-time event. PCI DSS requires continuous monitoring of your payment environment. Tools like Sansec actively monitor for Magecart-style script injections and supply chain attacks on Magento stores. Pair this with regular vulnerability scans and penetration testing to maintain your security posture between formal assessments.

Pro Tip: Set up automated alerts for any changes to scripts loaded on your payment pages. A Content Security Policy violation report endpoint gives you real-time notification of injection attempts. This is your early warning system for Magecart attacks.

For a broader view of proactive ecommerce security practices that complement payment gateway controls, the overlap between platform security and payment security is worth understanding.

Key takeaways

A secure payment gateway requires correct SAQ classification, 3DS2 integration with soft decline handling, and raw-body webhook verification to protect transactions and maintain PCI DSS compliance.

| Point | Details |

|---|---|

| SAQ classification matters | Merchant scripts on payment pages can shift scope from SAQ A to SAQ A-EP, increasing compliance obligations significantly. |

| Script control is mandatory | PCI DSS 4.x requires script inventories and tamper detection even for SAQ A merchants using hosted payment pages. |

| 3DS2 must handle all outcomes | Frictionless flows, challenge flows, and soft declines each require explicit handling to avoid lost sales and SCA failures. |

| Webhook security is technical | Signature verification must occur on raw request bytes before any JSON parsing to prevent production failures. |

| MFA scope is broader than expected | PCI DSS v4.0 requires MFA for all CDE access, including local and console access, not just remote logins. |

Why getting payment gateway security right is worth the effort

I have worked on enough eCommerce builds to know that payment gateway security is the area where merchants most often underestimate the complexity. The assumption is usually: “We are using Stripe, so we are covered.” That is partially true. Stripe’s infrastructure is secure. But your integration, your checkout page scripts, and your webhook handlers are your responsibility, and that is where the vulnerabilities live.

The PCI DSS 4.x changes around script control are genuinely significant. Requirements 6.4.3 and 11.6.1 caught a lot of merchants off guard when they came into full effect. The merchants who struggled most were those who had accumulated years of third-party tags on their checkout pages without a clear inventory. Cleaning that up retrospectively is painful. Building it correctly from the start takes a fraction of the effort.

On the SCA side, I think the industry has largely moved past the initial disruption of 3DS2 rollout. The exemption logic is well-understood now, and gateways like Adyen and Stripe handle a lot of the complexity for you. The remaining failure point is soft decline handling, and it is still surprisingly common to see integrations that treat a soft decline as a hard failure. That is lost revenue, full stop.

Looking ahead, W3C’s Secure Payment Confirmation draft is worth watching. It promises to move payment authentication beyond encryption towards verifiable user consent signals, which could meaningfully reduce friction for returning customers while strengthening security. It is not production-ready for most merchants yet, but it signals where browser-native authentication is heading.

My honest advice: treat your checkout architecture review as a security exercise, not just a development task. The decisions you make about which scripts run on your payment page, which gateway integration pattern you use, and how you handle authentication flows have compliance and revenue consequences that last for years.

— Steve

How Bigeyedeers can help with payment gateway integration

If you are building or re-platforming an online store and need payment gateway integration done properly, Bigeyedeers has the technical depth to get it right. We work across Magento and Shopify builds, handling everything from checkout architecture audits and PCI DSS scope definition to 3DS2 integration, webhook security, and ongoing compliance monitoring using Sansec.

We do not treat payment security as an afterthought. It is built into how we scope, design, and deliver every eCommerce project. Whether you are a growing DTC brand or an enterprise retailer managing complex B2B payment flows, we can help you implement a payment processing solution that is secure, compliant, and built to handle real transaction volumes. Get in touch with our team to discuss your requirements.

FAQ

What is a secure payment gateway?

A secure payment gateway is a technology service that encrypts and transmits payment data between a customer’s browser, the merchant’s store, and the acquiring bank, protecting card details and ensuring compliance with PCI DSS and SCA requirements.

What is the difference between SAQ A and SAQ A-EP?

SAQ A applies to merchants who fully outsource payment processing to a PCI DSS-compliant hosted page or iframe, with no merchant scripts touching payment fields. SAQ A-EP applies when merchant-controlled scripts on the checkout page can influence or interact with the payment form, which increases the compliance scope considerably.

How does 3DS2 affect the checkout experience?

EMV 3D Secure 2 enables frictionless authentication for low-risk transactions, meaning most customers will not see a challenge step. Higher-risk transactions trigger a step-up verification. Correctly handling soft declines and exemptions is critical to maintaining conversion rates while meeting SCA obligations.

Why does webhook signature verification fail in production?

The most common cause is JSON middleware processing the request body before the signature check runs. Signature verification must occur against the raw request bytes. Parsing the JSON first alters the byte representation and breaks the HMAC comparison.

Do I need MFA if I am not storing card data?

Yes. PCI DSS v4.0 requires multi-factor authentication for all access into the cardholder data environment, regardless of whether you store card data directly. This includes local, console, and application access, not just remote logins.

Recommended

Adobe Commerce (Magento)

Formerly known as Magento, Adobe Commerce is built for complex catalogues, integrations, and long term growth. We design and develop stable, scalable stores that support demanding eCommerce requirements, including multi-store setups, complex pricing, and Hyva based performance improvements.

Bespoke Build

We design and build custom eCommerce platforms for businesses with complex workflows, integrations, or non standard requirements. Built from scratch around your business needs using Laravel and modern architectures.

Working with brands across the UK from our offices in Cardiff and Exeter, you deal directly with a senior team of designers and developers specialising in Shopify, Magento, WordPress and bespoke eCommerce platforms.

We focus on commercial outcomes. Better conversion rates, strong SEO foundations and eCommerce platforms that continue to improve long after launch.